Name

MACD逃顶策略

Author

program

Strategy Description

介绍: MACD量价背离时卖出持有币种

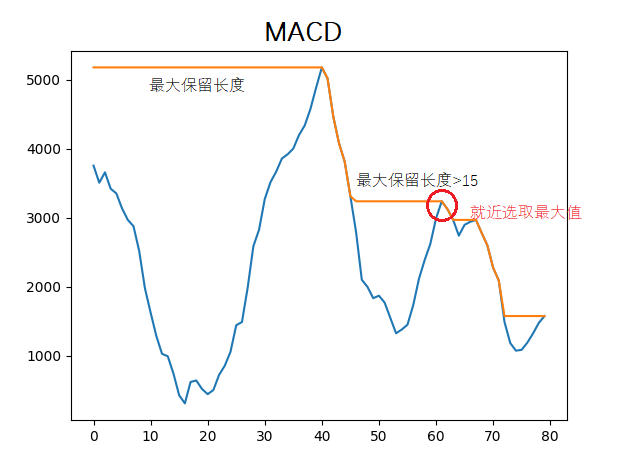

原理实现: 以当前macd值为开始向前遍历找出大于当前macd值的索引对应k线收盘价,锁定对应k线价格到当前收线k线范围内的最大值,如果当前价格大于区域内最高价则触发卖出。

向前遍历macd数据当最大保留长度大于15,就近选择macd最大值

说明: 策略只支持现货,可以多币种同时运行,源码仅供参考,实盘操作请谨慎运行。

Strategy Arguments

| Argument | Default | Description |

|---|---|---|

| num | 0.1 | 卖出数量 |

Source (python)

'''backtest

start: 2023-01-01 00:00:00

end: 2023-05-12 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Bitfinex","currency":"BTC_USD","stocks":10}]

'''

# from matplotlib import pyplot as plt

# plt.figure()

class ExitTop(object):

def __init__(self,index):

self.index = index

self.totestlist = [] # MACD数据

self.klist = [] # k线数据

self.toplus = []

self.tocpn = []

self.Sell = False

# 获取k线及MACD数据

def GetRecord(self) -> bool:

self.totestlist = []

self.klist = []

self.toplus = []

self.tocpn = []

records = exchanges[self.index].GetRecords()

macd = TA.MACD(records, 12, 26, 9)

# 判断DIF是否大于DEA

if not macd[0][-2] > macd[1][-2] and macd[0][-3] < macd[1][-3] or not macd[0][-2] > macd[1][-2] and macd[0][-4] < macd[1][-4]:

return False

self.totestlist = macd[0][len(macd[0])-80:]

# 封装k线数据

for get in range(len(records)):

self.klist.append(records[get]["Close"])

self.klist = self.klist[len(self.klist)-80:]

return True

def mepath(self):

if not self.GetRecord():

return False

# 向前遍历发现最大值

maxsign = -1000000000000

for i in range(len(self.totestlist)-1,-1,-1):

if self.totestlist[i] > maxsign:

maxsign = self.totestlist[i]

self.tocpn.append([1,i])

else:

if len(self.tocpn) > 0:

self.tocpn[-1][0] = self.tocpn[-1][0]+1

self.toplus.insert(0,maxsign)

sign = False

shorttime = [0,0] # 步长 , 索引

for i in range(len(self.tocpn)):

if self.tocpn[i][0] > 15 and sign == False:

shorttime = [self.tocpn[i][0],self.tocpn[i][1]]

sign = True

# 如果最大索引不是自己

if shorttime[1] < len(self.klist)-4:

# 锁定区域内最高价格

are = max(self.klist[shorttime[1]:-4])

# 判断是否存在大于当前macd值,如果当前价格大于区域内最高价格

if self.totestlist[-2]+300 < self.totestlist[shorttime[1]] and self.klist[-2] >= are:

return True

return False

return False

def main(self):

result = self.mepath()

if result == True and self.Sell == False:

exchanges[self.index].Sell(-1, num)

self.Sell = True

elif result == False:

if self.Sell == True:

self.Sell = False

# plt.plot(self.totestlist)

# plt.plot(self.toplus)

# LogStatus(plt)

def main():

transaction = []

for index in range(len(exchanges)):

transaction.append(ExitTop(index))

while True:

for tran in range(len(transaction)):

transaction[tran].main()

Sleep(1000*60)Detail

https://www.fmz.com/strategy/356399

Last Modified

2023-05-13 21:21:01