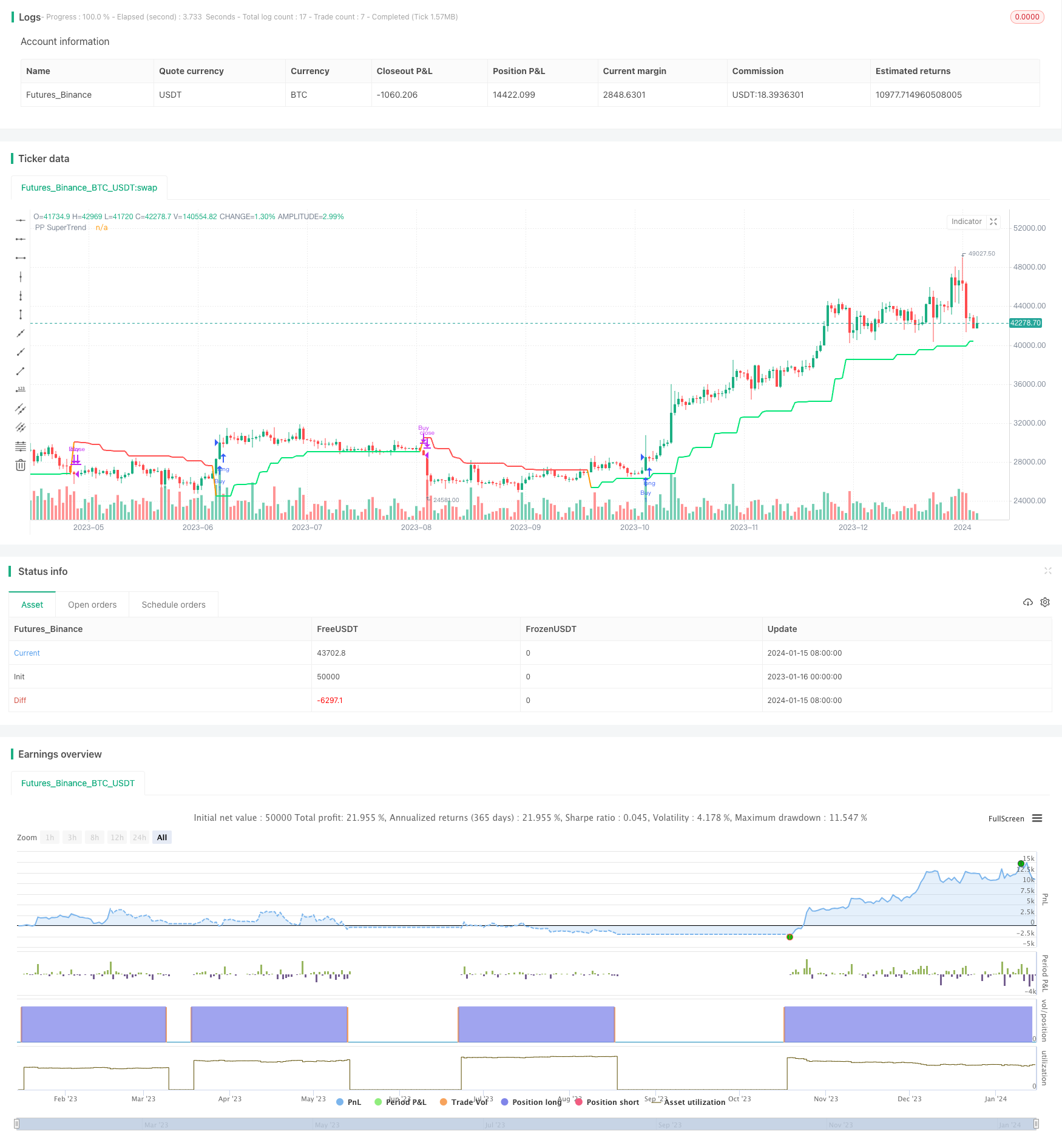

Name

趋势追踪移动止损策略Trend-Tracking-Trailing-Stop-Strategy

Author

ChaoZhang

Strategy Description

[trans]

趋势追踪移动止损策略是一种结合趋势判断指标和移动止损机制的量化交易策略。该策略运用超级趋势指标判断当前趋势方向,并利用移动止损线实时跟踪价格变化,实现趋势跟踪和风险控制。

该策略首先计算超级趋势指标,判断当前处于上升趋势还是下降趋势。超级趋势指标结合了ATR指标和中枢点,可以更准确地判断趋势方向。如果超级趋势指标判断为上升趋势,则产生买入信号;如果判断为下降趋势,则产生卖出信号。

在产生买入信号时,该策略会开仓做多;同时,它会实时计算一个移动止损线,该止损线的计算方式是中枢点减去ATR指标的数值。只要当前收盘价高于该止损线,止损线就会实时上移,始终保持在合理止损位置。如果价格跌破止损线,则平仓止损。

该策略同时结合ADX指标和RSI指标来过滤不合适的交易信号。只有在ADX大于设定阈值、RSI处于合理水平时,才会采信超级趋势指标的信号开仓。

该策略最大的优势在于能够很好地把握趋势方向,实现趋势跟踪。超级趋势指标比简单移动平均线更准确,能快速判断转折点。与此同时,移动止损机制可以自动调整止损位,最大限度锁住利润,有效控制风险。

另外,该策略加入ADX和RSI指标进行滤波,可以避免在市场波动较大的时期产生错误交易。ADX指标保证有足够的趋势性,RSI指标避免超买超卖现象,从而提高盈利概率。

该策略最大的风险在于趋势判断出错,超级趋势指标发出错误信号的概率。尽管超级趋势指标较简单移动平均线更优秀,但在复杂行情中也难免会判断失误。这时就需要依赖止损机制来控制损失。

此外,策略参数设置不当也会带来一定风险。例如ATR参数过大会导致止损线调整过于激进;ADX和RSI的参数设定不当也可能错过交易机会或者增加错误交易的概率。这需要通过大量历史回测来寻找最优参数。

该策略可以从以下几个方面进行进一步优化:

-

尝试其他趋势判断指标,如DMI、KDJ等,与超级趋势指标组合,形成“多因子”判断体系,可能可以提高判断准确率。

-

增加基于机器学习的自适应参数优化模块,使ATR参数、ADX参数、RSI参数等可以根据实时市场调整,而不是简单的固定值。

-

引入情绪指标等替代RSI指标,过滤信号。RSI指标对复杂行情的判断并不理想,而社交情绪指标等可以更好地判断市场热度。

-

增加仓位管理模块,根据止损线离当前价距离的远近,动态调整仓位大小。离止损线越远,可以适当加大仓位,提高盈利空间。

趋势追踪移动止损策略综合运用了趋势分析、移动止损和多因子过滤等方法,在捕捉趋势的同时严格控制风险,是一种较为成熟的量化策略。该策略优化空间还很大,值得进一步研究改进,使其适应更加复杂的市场环境。

||

The Trend Tracking Trailing Stop strategy is a quantitative trading strategy that combines trend judgment indicators and trailing stop mechanisms. This strategy uses the Supertrend indicator to determine the current trend direction, and utilizes a trailing stop line to track price changes in real time, achieving trend tracking and risk control.

The strategy first calculates the Supertrend indicator to judge whether the current trend is up or down. The Supertrend indicator incorporates the ATR indicator and pivot point to more accurately determine the trend direction. If the Supertrend indicator judges an uptrend, a buy signal is generated. If it judges a downtrend, a sell signal is generated.

When a buy signal is generated, the strategy will open a long position. At the same time, it calculates a trailing stop line in real time. The calculation method of this stop line is the pivot point minus the ATR indicator value. As long as the current closing price is higher than this stop line, the stop line will move up in real time and maintain a reasonable stop loss position. If the price breaks through the stop line, the position will be closed out with a stop loss.

The strategy also incorporates the ADX and RSI indicators to filter unsuitable trading signals. Only when the ADX is greater than the set threshold and the RSI is at a reasonable level will the signals from the Supertrend indicator be trusted to open positions.

The biggest advantage of this strategy is that it can grasp the trend direction well and achieve trend tracking. The Supertrend indicator is more accurate than simple moving averages and can quickly determine turning points. At the same time, the trailing stop mechanism can automatically adjust stop levels to maximize profit locking and effectively control risks.

In addition, the ADX and RSI indicators are added to the strategy for filtration, avoiding errors during periods of high market volatility. The ADX indicator ensures sufficient trend, and the RSI indicator avoids overbought and oversold scenarios, thereby improving profitability.

The biggest risk of this strategy is that the trend judgment goes wrong and the Supertrend indicator issues a wrong signal. Although the Supertrend indicator is superior to simple moving averages, it is inevitable that misjudgments will occur in complex market conditions. At this point, it is necessary to rely on stop loss mechanisms to control losses.

In addition, improper strategy parameter settings can also pose risks. For example, an ATR parameter that is too large will lead to overly aggressive stop-loss line adjustments. Improper settings of the ADX and RSI parameters may also miss trading opportunities or increase the probability of wrong trades. This requires extensive historical backtesting to find the optimal parameters.

The strategy can be further optimized in the following aspects:

-

Try other trend judgment indicators such as DMI and KDJ in combination with the Supertrend indicator to form a "multi-factor" judgment system, which may improve judgment accuracy.

-

Increase the machine learning based adaptive parameter optimization module so that the ATR parameter, ADX parameter, RSI parameter and so on can adjust according to the real-time market instead of fixed values.

-

Introduce sentiment indicators to replace RSI indicators for signal filtering. RSI indicators do not perform well in complex market conditions, while social sentiment indicators can better determine market enthusiasm.

-

Increase position sizing management module. According to the distance between the stop line and the current price, dynamically adjust the position size. The further away from the stop line, the greater the position size can be appropriately increased to improve profit potential.

The Trend Tracking Trailing Stop strategy comprehensively employs methods such as trend analysis, trailing stops, and multi-factor filtering. While capturing trends, it strictly controls risks and is a more mature quantitative strategy. There is still great potential for optimizing this strategy to adapt it to more complex market environments.

[/trans]

Strategy Arguments

| Argument | Default | Description |

|---|---|---|

| v_input_1_close | 0 | EMA Source: close |

| v_input_2 | 2 | Pivot Point Period |

| v_input_3 | 2 | ATR Factor |

| v_input_4 | 18 | ATR Period |

| v_input_5 | timestamp(1 Dec 2022) | Start Date |

| v_input_6 | timestamp(12 Jan 2023) | End Date |

| v_input_7_close | 0 | Source: close |

| v_input_8 | false | Offset |

| v_input_9 | 14 | length |

| v_input_10 | 30 | overSold |

| v_input_11 | 65 | overBought |

Source (PineScript)

/*backtest

start: 2023-01-16 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Bendre ADX Sup Trend", overlay = true)

///////////////////////////

// SuperTrend + Pivot Point

//////////////////////////

src = input(close, title="EMA Source")

PPprd = input(defval = 2, title="Pivot Point Period")

AtrFactor=input(defval = 2, title = "ATR Factor")

AtrPd=input(defval = 18, title = "ATR Period")

StartDate = input(timestamp("1 Dec 2022"), title="Start Date")

EndDate = input(timestamp("12 Jan 2023"), title="End Date")

var float ph = na

var float pl = na

ph := ta.pivothigh(PPprd, PPprd)

pl :=ta.pivotlow(PPprd, PPprd)

float center = na

center := center[1]

// float lastpp = ph ? ph : pl ? pl : 0.0

float lastpp = na(ph) ? na(pl) ? na : pl : ph

if lastpp > 0

if na(center)

center := lastpp

else

center := (center * 2 + lastpp) / 3

Up = center - (AtrFactor * ta.atr(AtrPd))

Dn = center + (AtrFactor * ta.atr(AtrPd))

var float TUp = na

var float TDown = na

Trend = 0

TUp := close[1] > TUp[1] ? math.max(Up, TUp[1]) : Up

TDown := close[1] < TDown[1] ? math.min(Dn, TDown[1]) : Dn

Trend := close > TDown[1] ? 1: close < TUp[1]? -1: nz(Trend[1], 1)

Trailingsl = Trend == 1 ? TUp : TDown

// Lines

linecolor = Trend == 1 and nz(Trend[1]) == 1 ? color.lime : Trend == -1 and nz(Trend[1]) == -1 ? color.red : na

plot(Trailingsl, color = linecolor , linewidth = 2, title = "PP SuperTrend")

bsignalSSPP = close > Trailingsl

ssignalSSPP = close < Trailingsl

///////

// ADX

//////

lenADX = 14

th = 14

TrueRange = math.max(math.max(high-low, math.abs(high-nz(close[1]))), math.abs(low-nz(close[1])))

DirectionalMovementPlus = high-nz(high[1]) > nz(low[1])-low ? math.max(high-nz(high[1]), 0): 0

DirectionalMovementMinus = nz(low[1])-low > high-nz(high[1]) ? math.max(nz(low[1])-low, 0): 0

SmoothedTrueRange = 0.0

SmoothedTrueRange := nz(SmoothedTrueRange[1]) - (nz(SmoothedTrueRange[1])/lenADX) + TrueRange

SmoothedDirectionalMovementPlus = 0.0

SmoothedDirectionalMovementPlus := nz(SmoothedDirectionalMovementPlus[1]) - (nz(SmoothedDirectionalMovementPlus[1])/lenADX) + DirectionalMovementPlus

SmoothedDirectionalMovementMinus = 0.0

SmoothedDirectionalMovementMinus := nz(SmoothedDirectionalMovementMinus[1]) - (nz(SmoothedDirectionalMovementMinus[1])/lenADX) + DirectionalMovementMinus

DIPlus = SmoothedDirectionalMovementPlus / SmoothedTrueRange * 100

DIMinus = SmoothedDirectionalMovementMinus / SmoothedTrueRange * 100

DX = math.abs(DIPlus-DIMinus) / (DIPlus+DIMinus)*100

ADX = ta.sma(DX, lenADX)

//////

// MA

/////

lenMA = 21

srcMA = input(close, title="Source")

// offsetMA = input(title="Offset", type=input.integer, defval=0, minval=-500, maxval=500)

offsetMA = input(0, title="Offset")

outMA = ta.sma(srcMA, lenMA)

//

// RSI

//

length = input( 14 )

overSold = input( 30 )

overBought = input( 65 )

price = close

vrsi = ta.rsi(price, length)

// Buy - Sell Entries

buy = bsignalSSPP and outMA < close and ADX > th

sell = ssignalSSPP

if (buy and vrsi > overBought)

// .order // Tuned version

strategy.entry("Buy", strategy.long)

// strategy.close("Sell", "close Sell")

if (sell) and (strategy.position_size > 0)

// strategy.entry("Sell", strategy.short)

strategy.close("Buy", "Close Buy")

// if(sell and vrsi < overSold )

// strategy.entry("Sell", strategy.short)

// if(buy) and (strategy.position_size > 0)

// strategy.close("Sell", "close Sell")

Detail

https://www.fmz.com/strategy/439039

Last Modified

2024-01-17 11:19:06