Name

基于枢轴点和斐波那契回撤的自动趋势追踪策略Pivot-Point-and-Fibonacci-Retracement-Based-Automatic-Trend-Following-Strategy

Author

ChaoZhang

Strategy Description

该策略基于枢轴点和斐波那契回撤比率自动识别股价的ABC波段,并给出长短仓信号。策略利用枢轴点判断股价波段,然后计算ABC波段之间的斐波那契回撤比例,如果符合一定条件就产生交易信号。

- 计算股票的枢轴高点和低点

- 判断价格是否从上一波段高点下落或从上一波段低点上涨

- 计算当前波段与上一波段之间的斐波那契回撤比例

- 如果上涨波段和下跌波段的回撤比例都在适当范围内,则判定可能形成ABC波段

- 在ABC波段确认后,做多时设置止损为C点位,止盈为1.5倍波动;做空时设置止损为A点位,止盈为1.5倍波动

- 利用枢轴点判断关键支撑阻力区域,提高信号准确率

- 应用斐波那契回撤识别ABC形态,自动捕捉趋势转换点

- 止盈止损清晰合理,避免出现巨大亏损

- 枢轴点和斐波那契回撤并不能保证每次都精确判断趋势转换点,可能出现误判

- C点和A点止损可能被突破,造成损失扩大

- 需要参数优化,比如斐波那契回撤比率的范围

- 可以结合更多技术指标辅助判断ABC形态,提高信号准确率

- 可以优化斐波那契回撤比率的范围,以适应更多市场情况

- 可以结合机器学习方法训练判断ABC形态的模型

该策略基于枢轴点判断关键支撑阻力区域,并利用斐波那契回撤比例自动识别ABC形态,在波段转折点给出长短仓交易信号。策略逻辑清晰简洁,止盈止损设置合理,能够有效控制风险。但是也存在一定误判风险,需要进一步优化和改进以适应更多市场情况。

||

This strategy automatically identifies ABC patterns in stock prices based on pivot points and Fibonacci retracement ratios, and generates long/short signals. It uses pivot points to determine price waves and calculates Fibonacci retracement ratios between ABC waves. If the ratios meet certain criteria, trading signals are generated.

- Calculate the stock's pivot high and low points

- Judge if the price has fallen from the previous high point or risen from the previous low point

- Calculate the Fibonacci retracement ratio between the current wave and previous wave

- If the retracement ratios of both up and down waves are within proper ranges, determine a potential ABC pattern

- After ABC pattern confirmation, set stop loss at Point C for long, and Point A for short. Set take profit at 1.5 times the price wave range.

- Pivot points identify key support/resistance levels to improve signal accuracy

- Fibonacci retracements catch trend turning points by identifying ABC patterns

- Clear profit/loss rules avoid huge losses

- Pivot points and Fibonacci retracements cannot ensure perfect identification of every trend turning point. Misjudgements may occur.

- Point C and Point A stops can be broken through, leading to larger losses

- Parameters like Fibonacci retracement ratio ranges need further optimization

- Incorporate more technical indicators to assist ABC pattern confirmation, improving signal accuracy

- Optimize Fibonacci retracement ratio ranges to suit more market conditions

- Utilize machine learning methods to train ABC pattern recognition models

This strategy identifies ABC patterns for generating long/short signals at trend turning points, based on pivot point confirmation of key support/resistance levels, and Fibonacci retracement ratio calculations. The logic is simple and clean, with sensible profit/loss rules that effectively control risks. However, certain misjudgement risks remain, requiring further optimizations and improvements to suit more market conditions.

[/trans]

Strategy Arguments

| Argument | Default | Description |

|---|---|---|

| v_input_1 | 5 | len |

Source (PineScript)

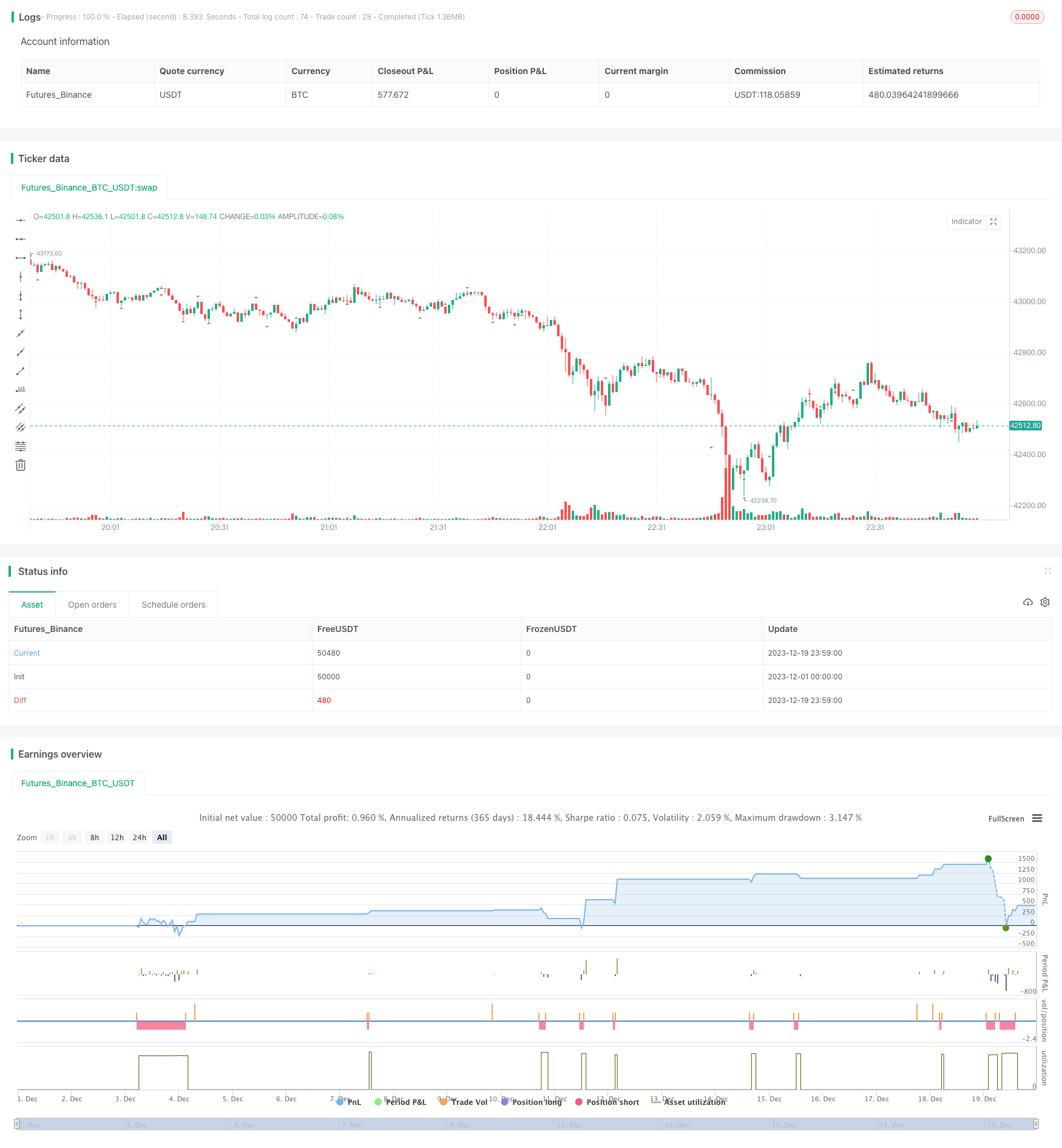

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-19 23:59:59

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © kerok3g

//@version=5

strategy("ABCD Strategy", shorttitle="ABCDS", overlay=true, commission_value=0.04)

calcdev(fprice, lprice, fbars, lbars) =>

rise = lprice - fprice

run = lbars - fbars

avg = rise/run

((bar_index - lbars) * avg) + lprice

len = input(5)

ph = ta.pivothigh(len, len)

pl = ta.pivotlow(len, len)

var bool ishigh = false

ishigh := ishigh[1]

var float currph = 0.0

var int currphb = 0

currph := nz(currph)

currphb := nz(currphb)

var float oldph = 0.0

var int oldphb = 0

oldph := nz(oldph)

oldphb := nz(oldphb)

var float currpl = 0.0

var int currplb = 0

currpl := nz(currpl)

currplb := nz(currplb)

var float oldpl = 0.0

var int oldplb = 0

oldpl := nz(oldpl)

oldplb := nz(oldplb)

if (not na(ph))

ishigh := true

oldph := currph

oldphb := currphb

currph := ph

currphb := bar_index[len]

else

if (not na(pl))

ishigh := false

oldpl := currpl

oldplb := currplb

currpl := pl

currplb := bar_index[len]

endHighPoint = calcdev(oldph, currph, oldphb, currphb)

endLowPoint = calcdev(oldpl, currpl, oldplb, currplb)

plotshape(ph, style=shape.triangledown, color=color.red, location=location.abovebar, offset=-len)

plotshape(pl, style=shape.triangleup, color=color.green, location=location.belowbar, offset=-len)

// var line lnhigher = na

// var line lnlower = na

// lnhigher := line.new(oldphb, oldph, bar_index, endHighPoint)

// lnlower := line.new(oldplb, oldpl, bar_index, endLowPoint)

// line.delete(lnhigher[1])

// line.delete(lnlower[1])

formlong = oldphb < oldplb and oldpl < currphb and currphb < currplb

longratio1 = (currph - oldpl) / (oldph - oldpl)

longratio2 = (currph - currpl) / (currph - oldpl)

formshort = oldplb < oldphb and oldphb < currplb and currplb < currphb

shortratio1 = (oldph - currpl) / (oldph - oldpl)

shortratio2 = (currph - currpl) / (oldph - currpl)

// prevent multiple entry for one pattern

var int signalid = 0

signalid := nz(signalid[1])

longCond = formlong and

longratio1 < 0.7 and

longratio1 > 0.5 and

longratio2 > 1.1 and

longratio2 < 1.35 and

close < oldph and

close > currpl and

signalid != oldplb

if (longCond)

signalid := oldplb

longsl = currpl - ta.tr

longtp = ((close - longsl) * 1.5) + close

strategy.entry("Long", strategy.long)

strategy.exit("Exit Long", "Long", limit=math.min(longtp, oldph), stop=longsl)

shortCond = formshort and

shortratio1 < 0.7 and

shortratio1 > 0.5 and

shortratio2 > 1.1 and

shortratio2 < 1.35 and

close > oldpl and

close < currph and

signalid != oldphb

if (shortCond)

signalid := oldphb

shortsl = currph + ta.tr

shorttp = close - ((shortsl - close) * 1.5)

strategy.entry("Short", strategy.short)

strategy.exit("Exit Short", "Short", limit=math.max(shorttp, oldpl), stop=shortsl)

Detail

https://www.fmz.com/strategy/437740

Last Modified

2024-01-05 11:34:17